%20(1).avif)

Europe

Africa

Venture capital is undergoing a reputation recalibration.

The last cycle rewarded speed, scale, and visibility.

This one rewards intentionality, alignment, and trust.

Capital markets have tightened. LP expectations have risen. Founders have become more selective than ever. In this new environment, the funds that stand out are those with the clearest beliefs, the strongest founder relationships, and the most coherent internal voice.

The End of a Decade of Expansion

For more than ten years, capital flooded into private markets. New funds launched monthly. Multi-stage platforms moved down-market. Sector specialisation blurred in an overcrowded landscape. But beneath the surface, a more consequential shift was forming:

Trust became the scarcest resource in venture capital.

Today’s downturn is not just cyclical; it is structural.

Global VC fundraising dropped to a six-year low in 2024 at $104.7B, an 18% decline year-over-year¹. In the U.S., fundraising volumes fell 62% with just one-third the number of funds closed compared to the previous cycle². LPs have concentrated their capital, backing fewer, higher-quality managers and allowing the long tail to fall away.

In a marketplace where capital no longer differentiates, vision, narrative, and trust do.

Thesis 1. Fund Performance: Not All Funds Are Good

The romantic idea that “capital always finds its way” collapses under real data. Venture capital is a power-law industry: roughly 60% of early-stage VC-backed companies fail to return cost, and 27% are written off entirely³. Because most funds rely on a handful of outlier wins, underperformance is widespread and often hidden, until it isn’t.

In the past 18 months, the cracks surfaced:

- OpenView, a respected SaaS investor, abruptly shut down months after raising a $570M fund⁴.

- CRV returned money to LPs, citing lack of viable opportunities and internal constraints⁵.

- Lakestar announced it would stop raising external capital altogether, shifting to a self-funded model⁶.

- Secondary buyers reported hundreds of LPs missing capital calls, threatening cascading risk across weaker funds⁷.

These events are not anomalies. They are symptoms of an industry where liquidity has stalled, valuations have compressed, and weaker platforms can no longer mask inconsistency.

The result is bifurcation:

A small number of highly credible funds thrive. Everyone else struggles to survive.

Thesis 2. Aligning LPs: Fundraising Has Become a Privilege

LP behaviour has transformed.

Where allocators once optimised for sector access, they now optimise for narrative coherence, governance, and long-term alignment.

The numbers illustrate the pressure:

- Global VC fundraising is down nearly 60% from its 2022 peak⁸.

- Q1 2024 was on track to be the lowest fundraising year since 2013⁹.

- Israeli funds saw a 74% YoY decline, the lowest since 2015¹⁰.

- Institutional LPs have “pulled back,” concentrating capital into the top tier¹¹.

- Weak exits have created a DPI bottleneck, limiting new commitments¹².

- Venture capital net cash flow has been negative for four consecutive years: a direct constraint on LPs’ ability to reinvest¹².

The conclusion is straightforward:

LPs haven’t stopped investing. They’ve stopped experimenting.

Funds with vague positioning, inconsistent communication, or superficial value-add claims are the first to be deprioritised.

Thesis 3. Aligning Founders: The Best Funds Create Opportunity, Not Just Capital

As capital becomes scarce, founders have become far more discerning.

The myth that “great founders take any term sheet” no longer holds. Data shows that founders actively seek investors who offer support far beyond capital — hiring, strategy, customer access, and operational guidance¹³,¹⁴,¹⁵,¹⁶.

In constrained markets, founders prioritise investors who:

- act as strategic partners,

- champion them in future rounds,

- integrate them into ecosystems,

- help them navigate difficult macro conditions.

Great founders now select their capital, not the other way around.

Reputation travels quickly. Founders compare notes. They know which firms truly support their companies, and which ones simply brand themselves as supportive.

A New World for Funds, Founders, and LPs

The convergence of performance bifurcation, LP consolidation, and founder selectivity is rewriting the rules of venture capital.

Founders no longer want the loudest investors; they want the most aligned.

LPs no longer optimise for scale; they optimise for conviction, coherence, and governance.

Both groups respond to narrative clarity, not headcount, fund size, or deal volume.

We are witnessing the rise of the Narrative Fund:

A fund whose ability to articulate belief, conviction, and purpose becomes a competitive advantage.

Visibility is not influence.

Being known is not the same as being trusted.

Across private capital, from pre-seed venture to sovereign-scale growth equity, the expectation is the same: communication must be coherent, credible, and continuous.

And the research reinforces it: Funds with clear communication around purpose and ESG orientation gain preferential access to high-quality deal flow¹⁷.

Funds that invest in structured narrative diffusion, consistent, cascading messaging, outperform peers¹⁸.

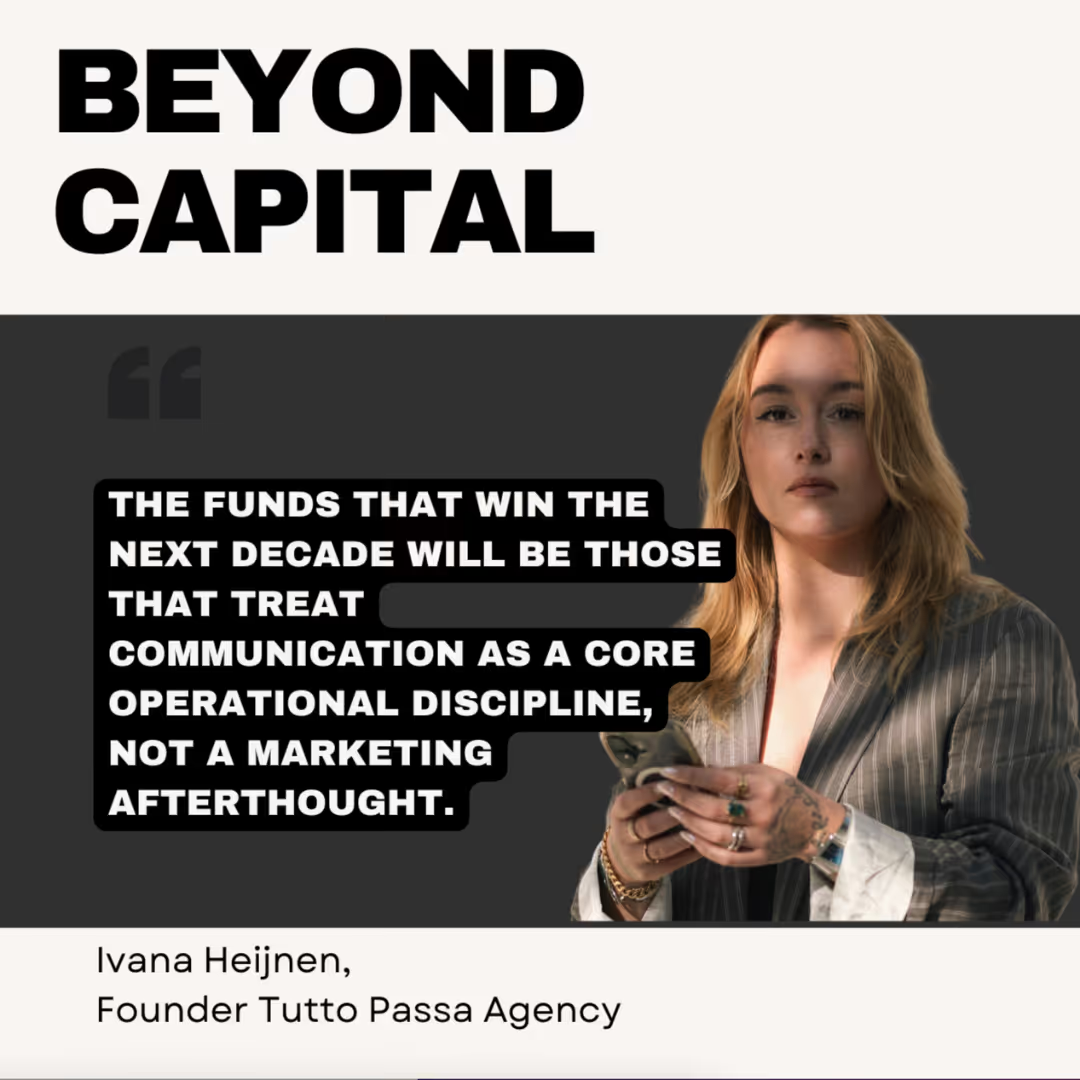

“The market no longer rewards the funds who shout the loudest. It rewards the funds who communicate with clarity, conviction, and continuity.”

Ivana Heijnen - Founder Tutto Passa Agency

References:

¹ Venture Capital Journal. (2024). Global VC fundraising hits six-year low.² Hustle Fund citing PitchBook/NVCA Q4 2023 Monitor.³ Vencap. (2023). Return of the Power Law.⁴ TechStartups. (2024). OpenView abruptly winds down operations.⁵ Business Standard / NYT. (2024). CRV to return money to LPs.⁶ Financial Times. (2024). Lakestar stops raising external capital.⁷ Business Insider. (2024). LPs defaulting on VC commitments.⁸ PitchBook. (2024). Global fundraising down nearly 60% from 2022.⁹ TechCrunch. (2024). Q1 fundraising on track for lowest year since 2013.¹⁰ Reuters. (2023). Israeli VC fundraising down 74%.¹¹ Confluence.VC. (2024). The shrinking LP appetite.¹² PitchBook IRR Report. (2022). VC IRR decline & write-downs.¹³ Copenhagen Business School. (2023). What founders value from VCs.¹⁴ Frontline Ventures. What Founders Want survey.¹⁵ VCStack. (2024). The Value-Add VC.¹⁶ Ventures Edge. (2024). More Than Capital.¹⁷ Dasgupta, Fos & Sautner. (2021). Institutional Investors and Corporate Governance.¹⁸ Chen & Kaur. (2023). Information Diffusion, Word-of-Mouth and Fund Performance.19 PitchBook. (2025). Why there’s no end in sight for venture capital’s liquidity crisis.

.avif)